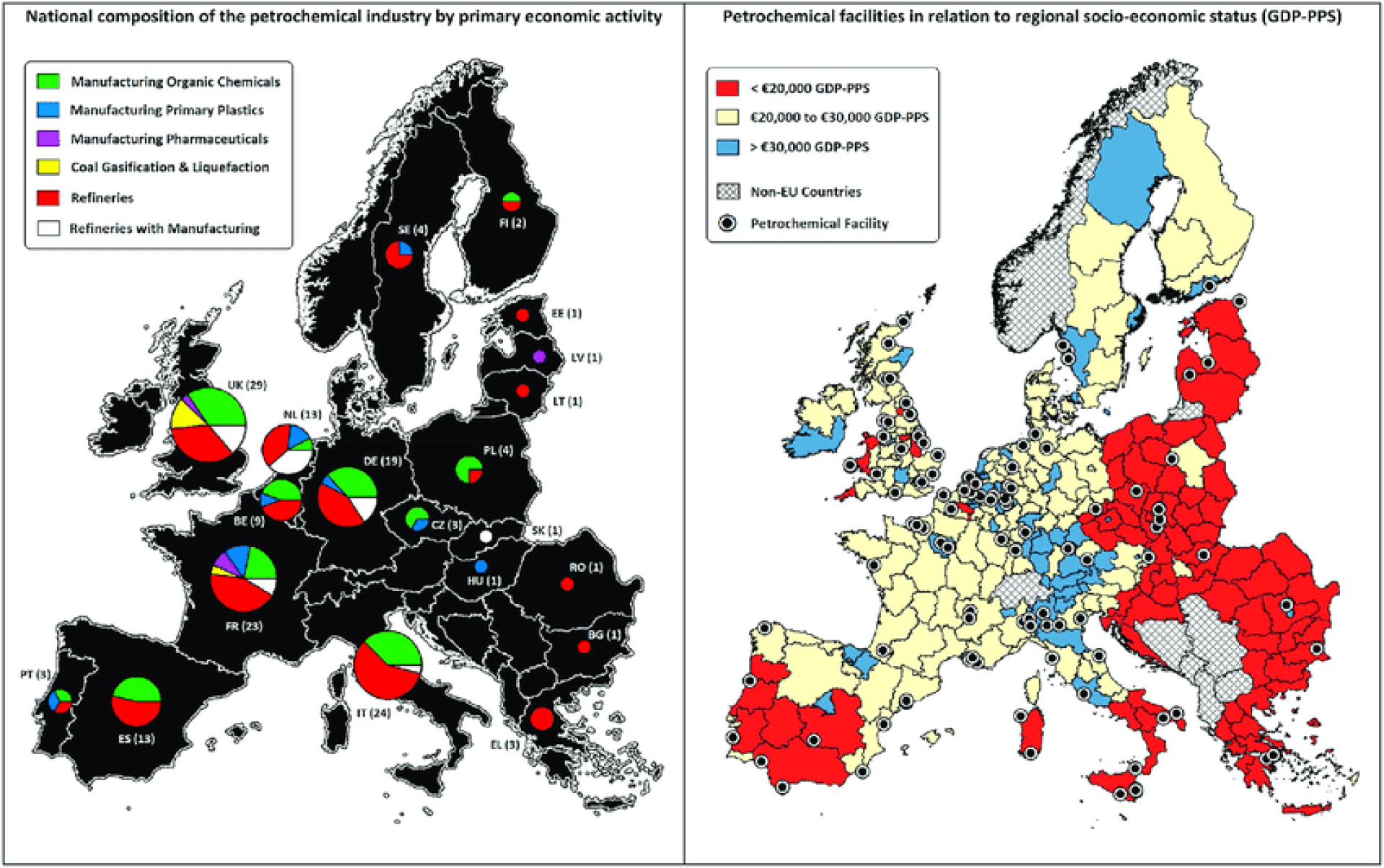

Europe's Petrochemical Industry Faces Historic Capacity Reduction

Europe's petrochemical industry is undergoing one of its most significant transformations in decades. Faced with rising energy costs, weak industrial demand, global oversupply, and increasing competition from lower-cost regions, producers across Europe are reducing capacity and restructuring operations. Major companies including ExxonMobil, TotalEnergies, Dow, and SABIC have announced plant closures, asset reviews, or production cutbacks as they seek to improve competitiveness in a challenging market environment.

The trend extends beyond individual facilities. Industry data shows that millions of tonnes of chemical and petrochemical capacity have been shut down, placed under review, or scheduled for closure since 2022. As a result, Europe is becoming increasingly dependent on imported petrochemical products, while producers in the Middle East, North America, and Asia continue to expand their global influence.